In global payment transactions, ensuring data security is a mandatory requirement. In the payment card industry in particular, the PCI DSS was established to help businesses build trust and credibility with customers while enhancing their competitive advantage.

So, what is PCI DSS? Why has it become an essential standard for major organizations in the payment ecosystem such as banks, financial institutions, and other payment-related entities? In this article, SQC Certification Vietnam will explore this topic in detail with you.

What is the PCI DSS Standard?

PCI DSS stands for Payment Card Industry Data Security Standard. It is a security standard designed to protect credit card information and reduce fraud risks in electronic payment transactions.

PCI DSS consists of a set of requirements developed to enhance the security of transactions involving payment cards such as credit cards and debit cards, while also protecting the personal information of cardholders.

The PCI DSS certification framework was established by the PCI Security Standards Council, an international organization founded in 2006 by five major global card brands:

- American Express

- Visa

- JCB International

- Mastercard

- Discover Financial Services

Origin of the PCI DSS Standard

The PCI DSS standard was developed as a security framework for organizations that store, process, or transmit payment card data. The creation of this standard is closely associated with the establishment of the PCI Security Standards Council (PCI SSC).

In the early 2000s, a series of payment card data breaches occurred worldwide, raising major concerns about the safety of card-based transactions. At that time, each card brand maintained its own security standard, which made global compliance difficult and inconsistent.

To address this challenge, in 2004, the five major card brands—Visa, Mastercard, American Express, Discover, and JCB—collaborated to establish a unified set of security requirements. This initiative led to the release of PCI DSS version 1.0.

In 2006, these five companies formally established the PCI Security Standards Council (PCI SSC) to develop and manage security standards for the payment card industry, with PCI DSS being the most prominent. The council itself does not perform audits or certifications, but instead provides standards, guidelines, and supporting resources.

The main objective of PCI DSS is to protect cardholder information throughout the payment processing lifecycle, thereby minimizing the risk of data breaches and card fraud while establishing a unified security standard for organizations operating in the payment ecosystem.

Organizations Required to Apply PCI DSS

The PCI DSS security standard applies to all organizations that interact with payment card data. Specifically:

1. Businesses Handling Payment Card Data

Any organization that processes, transmits, or stores payment card data (credit or debit cards) must comply with PCI DSS requirements.

These organizations can be large enterprises or small businesses, as the standard applies regardless of company size.

2. Merchants Accepting Card Payments

Companies, retail stores, and e-commerce websites that accept card payments for products or services are required to comply with PCI DSS.

Note:

Even if the payment processing is outsourced to a third-party provider, the merchant still retains responsibility for PCI DSS compliance.

3. Third-Party Payment Service Providers

These include organizations that support payment infrastructure or participate in the processing of cardholder data, such as:

- Payment gateways

- Hosting service providers

- IT infrastructure providers supporting payment systems

These organizations may store, process, or transmit cardholder data on behalf of merchants or customers, and therefore must comply with PCI DSS requirements.

4. Organizations with Dual Roles

Some organizations both sell goods/services and provide payment processing services for other businesses.

These entities must meet all applicable PCI DSS requirements for both roles.

Objectives of the PCI DSS Standard

The main objective of PCI DSS is to optimize the protection of sensitive payment cardholder data, such as credit card numbers, expiration dates, and security codes. By doing so, it helps organizations minimize the risk of data breaches, fraud, and cardholder information theft. In addition, the standard aims to achieve several broader goals:

Protect Cardholder Data

PCI DSS helps prevent the leakage or theft of credit and debit card information during storage, processing, and transmission.

Reduce Payment Fraud

When organizations properly implement PCI DSS requirements, they can significantly reduce the risk of cyberattacks, skimming, malware infections, and other financial fraud activities.

Establish a Global Security Standard

Compliance with PCI DSS provides a common security framework for all organizations participating in the payment card ecosystem worldwide.

Strengthen IT Security Controls

The standard requires organizations to implement strong security mechanisms such as firewalls, data encryption, access control, system monitoring, and regular security testing.

The 12 Security Requirements of PCI DSS

The PCI DSS standard establishes a comprehensive set of security principles and requirements designed to protect payment card data. Its primary goal is to ensure that all processes involving card data storage, transmission, and processing occur within a secure environment, minimizing the risk of data leaks and regulatory violations.

The standard includes 12 core requirements, supported by more than 280 detailed sub-requirements, which are organized into six major security objectives. Below are the 12 core PCI DSS security requirements:

1. Install and Maintain Firewall Configurations to Protect Cardholder Data

Firewalls serve as the first line of defense between internal networks and external public networks. Organizations must establish and maintain proper firewall configurations to control traffic and prevent unauthorized access.

2. Do Not Use Vendor-Supplied Default Security Settings

Default passwords and security settings provided by vendors create significant security risks. Organizations must change all default credentials and configurations to strengthen system protection.

3. Protect Stored Cardholder Data

Stored cardholder data must be encrypted and strictly controlled. Even if attackers gain unauthorized access, the data cannot be interpreted without the proper decryption keys.

4. Encrypt Transmission of Cardholder Data Across Open Public Networks

Cardholder data must be strongly encrypted when transmitted across open networks such as the Internet, preventing interception and unauthorized decryption by third parties.

5. Use and Regularly Update Anti-Virus Software

Malware poses a major threat to sensitive data. Organizations must deploy anti-virus or anti-malware solutions and keep them regularly updated to detect and block emerging threats.

6. Develop and Maintain Secure Systems and Applications

Organizations must adopt secure software development practices, perform code reviews, and promptly patch vulnerabilities to prevent exploitation.

7. Restrict Access to Cardholder Data Based on Business Need-to-Know

Access to cardholder data should be granted only to individuals whose job roles require it, reducing the risk of internal data exposure.

8. Assign a Unique ID to Each Person with Computer Access

Each user must have a unique identification ID, enabling accurate tracking, monitoring, and accountability for actions performed within the system.

9. Restrict Physical Access to Cardholder Data

Organizations must ensure that physical storage locations for cardholder data are secured, monitored, and accessible only to authorized personnel.

10. Track and Monitor All Access to Network Resources and Cardholder Data

System activity logs and monitoring mechanisms must be implemented to detect unauthorized access or suspicious behavior in a timely manner.

11. Regularly Test Security Systems and Processes

Organizations must conduct vulnerability scans, penetration testing, and regular security assessments to identify and address potential weaknesses.

12. Maintain an Information Security Policy for All Personnel

Security is not only about technology but also about people. Employees must be trained and made aware of security policies and procedures to build a strong organizational culture of data protection.

PCI DSS Compliance Levels

According to the regulations of the PCI Security Standards Council, organizations that comply with PCI DSS are categorized into four compliance levels based on the number of payment card transactions processed annually, including both online and in-person transactions.

Each level has its own validation and assessment requirements to ensure that organizations maintain appropriate security controls when handling payment card data.

Level 1: PCI DSS Level 1

Applies to organizations that process more than 6 million card transactions per year.

This is the highest compliance level. Organizations must undergo a comprehensive annual assessment conducted by a qualified security assessor (QSA).

In addition, the organization must perform regular vulnerability scans conducted by an Approved Scanning Vendor (ASV) to quickly detect and mitigate security risks.

Level 2: PCI DSS Level 2

Applies to organizations processing between 1 million and 6 million transactions per year.

Organizations at this level are required to complete an annual Self-Assessment Questionnaire (SAQ) to demonstrate compliance.

They may also be required to perform quarterly vulnerability scans by an ASV, depending on the requirements of their acquiring bank.

Level 3: PCI DSS Level 3

Applies to organizations processing between 20,000 and 1 million transactions per year.

Similar to Level 2, organizations must complete an annual SAQ and may be required to perform quarterly ASV scans to maintain compliance.

Level 4: PCI DSS Level 4

Applies to organizations processing fewer than 20,000 e-commerce transactions annually.

Although this is the smallest category, Level 4 organizations are still required to complete the annual SAQ and may be required to conduct network vulnerability scans to ensure payment data security.

Benefits of PCI DSS for Businesses

Implementing PCI DSS compliance is not only a mandatory requirement for organizations handling payment card data, but also a strategic approach to strengthen internal information security capabilities.

Although the process may require significant technical effort and resource investment, it provides many important benefits for organizations.

1. Protection of Customer Payment Card Data

Organizations that successfully implement PCI DSS can establish multi-layered security controls, including:

- Data encryption

- Firewalls

- Role-based access control

- Access monitoring

- Regular security testing

These measures ensure that sensitive cardholder information such as PAN, CVV, and expiration date is strictly protected throughout the entire data processing lifecycle.

As a result, organizations can significantly reduce the risk of data breaches, card theft, and unauthorized system access, allowing customers to perform online transactions with confidence.

2. Increased Trust and Brand Reputation

PCI DSS certification or compliance demonstrates that an organization prioritizes customer data security through the implementation of internationally recognized security standards and technologies.

This helps build a strong reputation among customers, business partners, and financial institutions.

3. Strengthened Customer Confidence

Meeting PCI DSS security requirements shows that a company is committed to protecting customer data, which reinforces customer trust and encourages secure online payment adoption.

4. Reduced Cybersecurity Risks

Organizations implementing PCI DSS can proactively identify and remediate security vulnerabilities before they can be exploited by attackers.

This significantly reduces the risk of cyberattacks, financial fraud, regulatory penalties, and liability for data breaches.

5. Compliance with International Card Schemes and Banking Requirements

Compliance with PCI DSS is a mandatory requirement imposed by major global card networks such as: Visa, Mastercard American Express, JCB, Discover Financial Services

Meeting this requirement enables organizations to connect their systems with banks and financial institutions for payment card processing.

6. Expansion into Domestic and International Markets

PCI DSS can be considered a “security passport” that enables businesses to participate in the global payment ecosystem.

Compliance makes it easier for organizations to collaborate with:

- international partners

- global e-commerce platforms

- international payment gateways

- financial investors and B2B customers

Many international partners require PCI DSS compliance as a prerequisite for business cooperation.

7. Alignment with Industry Best Practices

Compliance with PCI DSS means that an organization is adopting industry-recognized security best practices.

This enhances credibility with partners, service providers, regulators, and financial institutions, demonstrating that the organization maintains a mature and responsible approach to information security.

Risks of Not Implementing PCI DSS

When an organization fails to comply with the requirements of the PCI DSS, it may face several significant risks:

1. Card Data Breaches and Theft

Cardholder information can be exploited by hackers if proper security controls are not implemented.

This may lead to financial fraud, identity theft, and significant financial losses for both customers and the organization.

2. Financial Penalties and Liability

Failure to comply with PCI DSS may result in financial penalties imposed by acquiring banks or major card brands, such as:

- Visa

- Mastercard

Organizations may also be required to pay compensation for damages and may face increased transaction processing fees.

3. Loss of Card Payment Processing Privileges

A non-compliant business may have its card payment processing privileges suspended or revoked, meaning the company will no longer be able to accept credit or debit card payments.

4. Damage to Brand Reputation

Security incidents or data breaches can lead to loss of trust from customers and business partners, causing long-term damage to the organization’s reputation and brand image.

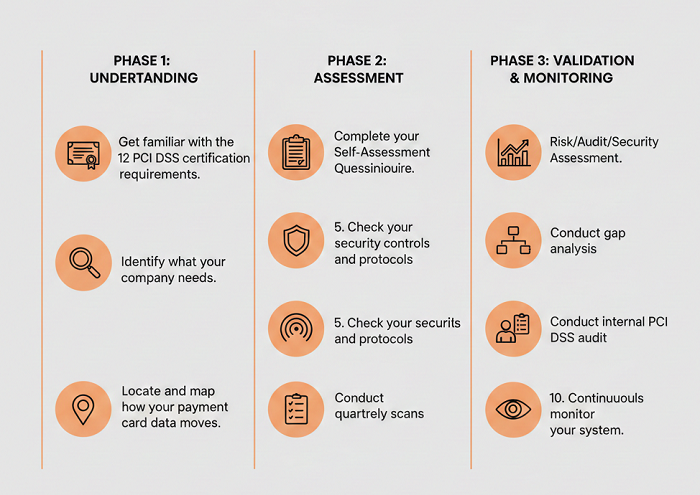

11 Steps to Achieve PCI DSS Certification

To obtain PCI DSS certification, organizations typically undergo an assessment conducted by a Qualified Security Assessor Company (QSAC).

The certification process requires organizations to comply with all 12 PCI DSS requirements and maintain ongoing security practices.

Below are 11 logical steps toward achieving PCI DSS compliance:

1. Meet the 12 Core PCI DSS Requirements

Organizations must implement the 12 core PCI DSS security requirements, including firewalls, card data protection, encryption, and access control.

2. Determine the Organization’s PCI DSS Level

Identify the appropriate PCI DSS compliance level (Level 1–4) based on the total number of card transactions processed annually.

3. Define Scope and Map Cardholder Data Flow

Establish the PCI DSS scope and create cardholder data flow diagrams showing how card data is collected, processed, transmitted, and stored.

4. Conduct Risk Assessment of the Payment Environment

Identify vulnerabilities, security weaknesses, and potential threats within the payment infrastructure.

5. Perform a Gap Analysis

Compare the organization’s current security posture with PCI DSS requirements to identify missing controls.

6. Implement Required Security Controls

Deploy necessary security technologies and policies, such as TLS encryption to protect card data during transmission.

7. Conduct External Vulnerability Scanning

Perform internal and external vulnerability scans, including scans conducted by Approved Scanning Vendors (ASV).

8. Maintain Continuous Monitoring

Continuously monitor systems, maintain logs, and submit periodic reports to card brands and acquiring banks.

9. Complete the Self-Assessment Questionnaire (SAQ)

Fill out the appropriate SAQ form based on the organization’s payment processing model.

10. Conduct Internal PCI DSS Readiness Assessment

Perform an internal audit or readiness assessment before the official certification audit to minimize compliance gaps.

11. Undergo QSA Assessment

A Qualified Security Assessor (QSA) will evaluate the entire cardholder data environment (CDE) and issue the official Report on Compliance (ROC) if requirements are satisfied.

Challenges in Implementing PCI DSS

Organizations operating in finance, payments, or any environment that processes payment card transactions often face several challenges when implementing PCI DSS.

1. Implementation Complexity

PCI DSS contains many technical requirements and complex security controls, which can be difficult to implement—especially for small and medium-sized organizations with limited expertise and resources.

2. High Implementation Costs

Maintaining PCI DSS compliance requires significant investment, including:

- Security technologies

- System upgrades

- Staff training

- Periodic assessments and audits

3. Continuous Compliance Requirements

PCI DSS compliance is not a one-time activity.

Organizations must continuously monitor, maintain, and update their security environment to remain compliant.

4. Rapidly Evolving Threat Landscape

Cybersecurity threats are constantly evolving, and PCI DSS standards are regularly updated to address new risks.

Organizations must therefore continuously adapt their security controls to avoid becoming non-compliant with updated requirements.

PCI DSS Certification Services by SQC Certification Vietnam

SQC Certification is one of only three organizations in Vietnam authorized by the PCI Security Standards Council (PCI SSC) to conduct PCI DSS certification assessments for enterprises across the Asia-Pacific (APAC) region.

SQC’s capabilities include authorization to perform the following PCI DSS activities:

- Conduct PCI DSS compliance assessments

- Issue PCI DSS certification

- Provide consulting and support for implementing security controls to protect cardholder data

- Deliver PCI DSS training programs

PCI DSS certification is not merely a certificate—it represents a strong commitment by an organization to security, transparency, and professionalism in protecting payment card data.

Clients using the services of SQC Certification Vietnam will receive:

- A scientific, transparent, and professional assessment process

- Streamlined procedures with full support throughout the certification journey

- All-inclusive pricing with no unexpected additional costs

- 24/7 support services with dedicated and responsible assistance

- Attractive after-sales policies, including exclusive incentives for loyal customers

We hope the information shared above has helped you better understand what PCI DSS is. Let SQC Certification Vietnam support your organization in achieving international standards in a professional and sustainable manner.

- Hotline: 093.639.6611

- Website: https://sqccert.com.vn/

- REGISTER NOW: https://forms.gle/ydn9rzk5H7jrrf9g9

What is a SOC 2 Report? A Guide to SOC 2 Reporting for Technology Businesses

What is a SOC 2 Report? A Guide to SOC 2 Reporting for Technology Businesses Latest Updates to SOC 2 for Businesses in 2026

Latest Updates to SOC 2 for Businesses in 2026 Free Training Course: HIGG FEM Assessment Toolkit and Latest Updates

Free Training Course: HIGG FEM Assessment Toolkit and Latest Updates SQC Certification Vietnam officially becomes a QSAC authorized by PCI SSC.

SQC Certification Vietnam officially becomes a QSAC authorized by PCI SSC. What is a QSA? The Role of a QSA in the PCI DSS Assessment Process

What is a QSA? The Role of a QSA in the PCI DSS Assessment Process Comparison of ISO 27001 vs ISO 27002: Similarities and Differences

Comparison of ISO 27001 vs ISO 27002: Similarities and Differences